Originally published March 6, 2018. Updated May 30, 2024.

Plan N is often a hot topic among independent insurance agents. Is it worth the risk, especially when you put it up against a Plan G?

Let's take a look at premium savings, copays, excess charges, rate increases, and more.

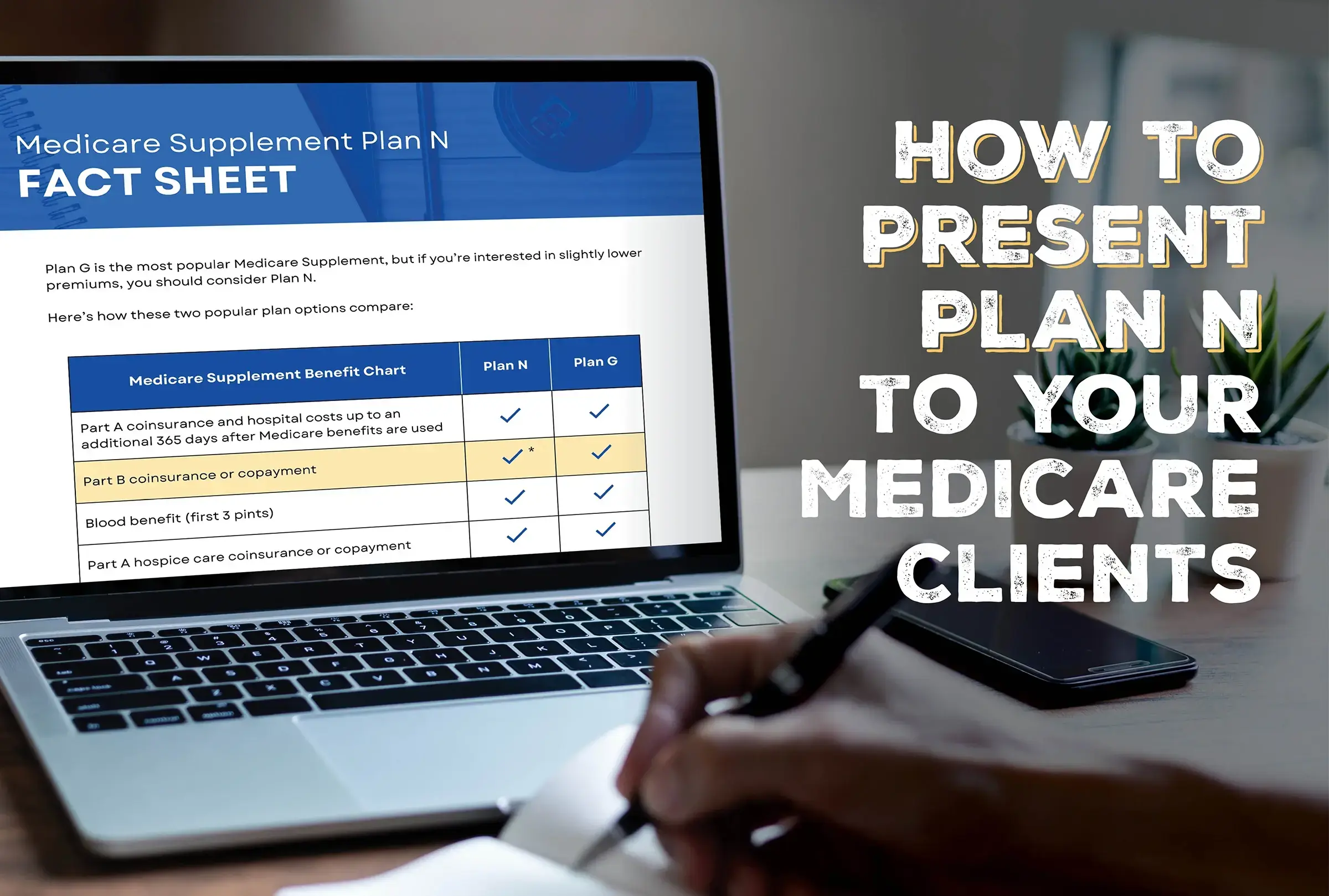

Use the Plan N Fact Sheet

Before we get into all the Plan N details, I want to ensure you have a copy of the Plan N Fact Sheet.

This will help you present and explain Plan N to your clients so they can understand it.

It's a one-page sheet, front and back, that walks your client through:

- Plan N vs. Plan G

- How copays work

- What excess charges means (with an example)

- The perks of Plan N

If you've been wanting to offer Plan N to your clients but feel like they'll just get confused, this fact sheet may be your golden ticket.

Learn more about the fact sheet in this blog post: How to Present Plan N to Your Medicare Clients

Is the Plan N premium low enough to be worth it?

The big upside to Medicare Supplement Plan N is the lower premium compared to Plan G.

The severity of the cost savings depends on where you’re selling, but in several areas we analyzed, Plan N averaged out to about 28% cheaper.

Plan N also often has the benefit of being well under $100. And that's not just for T65s – we see under $100 premiums for Plan N through the mid-70s age range.

The left-digit bias makes even $99 seem significantly less than $100, so premiums in $75-$80 range is definitely enough to turn heads!

What about Plan N copays?

Unlike G, Plan N does have copays. The copays are up to $20 for some office visits and up to $50 for emergency room visits that don’t result in inpatient admission.

While Plan G doesn’t have copays, which simplifies things, the thought of copays isn’t necessarily a dealbreaker for clients. Most major medical plans have copays, so your clients are probably used to them.

However, if the client is constantly in and out of the doctor, there comes a point where it’s more cost-effective to have a Plan G.

It's worth asking:

- Is the premium difference between a G and N significant enough to make sense for the client?

- Would the client rather not fuss with additional medical bills, even if it means paying a little extra for the monthly premium?

Related: 2024 Plan F Agent Guide

What about excess charges?

Most doctors and providers accept Medicare assignment, meaning they agree to pay a Medicare-approved amount for a certain service.

For example, a doctor might charge $1,500 for a procedure, but Medicare only approves $1,200 for that procedure. If the doctor accepts assignment, they’ll lower their billing rate to the approved $1,200. If they don’t accept assignment, the patient will receive a bill in the form of an excess charge.

Here's how Medicare.gov defines an excess charge:

“If you have Original Medicare, and the amount a doctor or other health care provider is legally permitted to charge is higher than the Medicare-approved amount, the difference is called the excess charge.”

The issue with Medigap Plan N is that excess charges are not covered, while Plan G does cover excess charges.

Excess charges are unlikely

The thought of the unknown can be troubling to seniors, but it’s important to realize that most doctors accept Medicare assignment.

Depending on what source you look at, the percentage of doctors who accept Medicare assignment ranges from 93-98%.

To avoid any excess charge bills, all your client has to do is ask if their doctor accepts Medicare assignment before ever going in for a visit.

Is the hassle factor worth the savings?

But again, excess charges is another potential point of confusion for your client. Would they rather not have to worry about excess charges in exchange for the slightly higher premium of Plan G?

In many cases, a client might put a price tag on the potential “hassle factor” of additional medical bills. I know plenty of people who would rather pay a higher premium to avoid the hassle of copays and excess charges.

But I also know even more people who would gladly take on that hassle for a 28% average premium savings.

What about rate increases?

When looking at all of the most popular Medicare Supplement plans, Plan N does have a more welcoming rate increase history.

If you're trying to set your clients up for the long run, future rate increases are definitely a factor to consider.

In 2018, David Friedman, Aetna’s Regional Sales Manager for the Midwest said, “Plan N has lower rate increases year over year – especially in Aetna’s portfolio.”

I've talked to many industry experts as of 2024, and that statement is definitely holding true. Plan N has even seen some rate reductions over the last year!

Because Plan N is not a Guaranteed Issue plan (Plan G is now), the claims experience is much more favorable. Carriers can keep rates down by having a healthier pool of policyholders, overall.

Premium savings benefits

When you show your client the premium savings of a Plan N compared to a Plan G, it's much easier to cross-sell additional coverages to meet their needs.

For example: "If you chose Plan N, you'd be saving $25 per month compared to a Plan G – we could add $20,000 of cancer insurance coverage for about that price!"

Consider the value you just added for your client for the same price as a Plan G.

Agent benefits

Plan N also has benefits for the agent!

The commission on Plan N is usually higher than other plans. Because Plan N is not a Guaranteed Issue (GI) plan, the claims experience is so much lower for the carrier. The rates stay better and premiums stay more stable because of that.

They can reward policyholders with much lower premiums and agents with higher commissions because of it.

In fact, carriers are even offering cash bonus programs to agents just for selling Plan N. Now is certainly the time to jump on board!

Conclusion

In many cases, a Plan G is easier to understand, which makes it easier to present to a client.

But at the end of the day, your job is to present the options to your client and let them make their own decision.

What are your thoughts on Plan N? Do you think it’s a good deal for your client?

Comments