Did you know 16% of individuals with Medicare coverage are under age 65 (Kaiser Family Foundation)?

Whether it's a mental disorder, an injury, cancer, or something else, those who are disabled will become eligible for Medicare benefits after a certain timeframe.

As an independent agent in the senior market, you are equipped to help those who are disabled and are under age 65. It's just a matter of knowing the rules in your state and navigating them.

That said, keep in mind that these state-specific regulations are constantly changing with new and pending legislation. So, while we've done a ton of homework here for you, give us a call if you have any specific questions or scenarios. We'll find out the answer for you (888-780-7676).

Qualifying for Medicare Disability

In order to qualify for Medicare benefits, your client must be getting disability benefits from Social Security or the RRB for 24 months. Also, those with ESRD or ALS (Lou Gehrig's disease) automatically qualify (Medicare.gov). This qualification criteria is the same for all states.

For those collecting disability benefits, on the 25th month, they'll be automatically enrolled in Medicare Parts A and B.

They'll get their Medicare card in the mail 3 months before their 25th month of disability. The process is just like those aging in to Medicare.

Under 65 Original Medicare Costs

Medicare tells us that if you're under 65, you can get premium-free Part A if you got Social Security or RRB disability benefits for 24 months. So, most disabled people you help under age 65 will have $0 premium for Part A.

No matter your age, you still must pay the Part B premium, which is $144.60 in 2020.

You can get a Medicare Supplement, but that's state-specific. For example, in Illinois, you can, but in Arizona, you can't.

%20Beneficiaries%2c%20Ages%2018-64.png?width=1550&name=Total%20Disabled%20Social%20Security%20Disability%20Insurance%20(SSDI)%20Beneficiaries%2c%20Ages%2018-64.png)

Total Disabled Social Security Disability Insurance (SSDI) Beneficiaries, Ages 18-64; Timeframe: 2013-2018 (KFF)

Those rules are also fluctuating constantly with new legislation. For example, in Indiana, Medigap carriers will have to offer at least Plan A on a GI basis starting in July 2020.

You can also purchase a Part D drug plan – the process is the same for under 65 as it is for those 65+.

Related: Medicare Basics for New Senior Market Insurance Agents

Under 65 Medicare Supplements

Federal rules don't guarantee access to Medigap plans for enrollees under age 65.

However, most states have some kind of regulations that make sure at least some Medigap plans are available (MedicareResources.org).

In the states that don't require Medigap carriers to offer plans, some carriers decide to anyway. For example, United American voluntarily chooses to offer some Medigap plans in states like Alabama, Iowa, Nebraska, and West Virginia.

But beware – the premiums are several times higher than premiums for 65-year-olds.

Are Medigap plans available in my state for those under 65?

Every state has its own regulations about Medigap plans and whether or not carriers have to offer it to those under 65.

We have a lot of agents licensed in multiple states, so we've read the fine print for you. Here's a quick, scannable list of Medigap plan availability by state.

A few quick notes: A few states have something called a high-risk pool. This offers supplemental coverage to Medicare beneficiaries who can't get a private Medicare plan. Those states are Alaska, Iowa, Nebraska, New Mexico, North Dakota, South Carolina, Washington, and Wyoming.

Also, three states have waivers from the federal government allowing them to have their own Medigap standardization. That includes Wisconsin (basic plan with riders), Minnesota (basic, basic with riders, extended basic, etc), and Massachusetts (Medicare Core and Med Supp 1).

Guide:

✅: Yes

⚠️: Yes, but options are very limited or there's pending legislation.

❌: No

- Alabama: ⚠️– only two carriers offer Medigap plans to those under 65 – Blue Cross Blue Shield of Alabama (Plan A) and United American (Plan B).

- Alaska: ❌

- Arizona: ❌

- Arkansas: ✅

- California: ⚠️– Medigap carriers are required to offer coverage to people under 65, but not if they have ESRD.

- Colorado: ✅

- Connecticut: ✅– carriers must offer Plans A, B, and/or C; prices are the same for everyone, whether you're under age 65 or not (community rated).

- Delaware: ✅ – there are separate rate pools for people with disabilities and people with ESRD (ESRD is much more expensive).

- District of Columbia: ⚠️– United American offers Plan B (very expensive).

- Florida: ✅

- Georgia: ✅

- Hawaii: ✅

- Idaho: ✅– something to note: premiums are limited to 150% of age-65 premiums.

- Illinois: ✅

- Indiana: ⚠️– as of July 2020, Medigap insurers in Indiana will have to offer at least Plan A on a GI basis.

- Iowa: ⚠️– Wellmark offers Plan A on a GI basis (it's expensive), and United American offers plan for under 65, but you have to go through underwriting.

- Kansas: ✅– those under 65 have the same access and premiums as those who are aging in to Medicare.

- Kentucky: ✅– not required by law, but several carriers offer a wide variety of plans, and the pricing is more reasonable than in other states.

- Louisiana: ✅

- Maine: ✅– plus, carriers can't vary premiums based on age, and that includes people under 65.

- Maryland: ✅– Medigap carriers are required to offer Plan A and Plan C, if they offer it.

- Massachusetts: ✅ – carriers can't charge higher premiums for under 65; carriers don't have to offer plans to those with ESRD.

- Michigan: ✅– carriers are required to offer Plans A, D, and G on a GI basis year-round for those under 65.

- Minnesota: ✅– their own Medigap plan types are available to people under 65, and carriers can't charge more for it.

- Mississippi: ✅– carriers are required to offer all plans to people under 65.

- Missouri: ✅– rates are equal to the weighted average rates for people age 65+.

- Montana: ✅

- Nebraska: ⚠️ – only United American, Plans A and B – very expensive ($5-7,000/yr).

- Nevada: ❌

- New Hampshire: ✅

- New Jersey: ✅– carriers must offer Plan D, and the price can't be more than those aging in to Medicare. The rules are slightly different for those who are disabled under age 50.

- New Mexico: ❌

- New York: ✅– prices are the same for everyone, whether you're under age 65 or not (community rated).

- North Carolina: ✅– carriers must offer Plan A, plus Plans C and F if they offer it

- North Dakota: ⚠️ – carriers don't have to offer Medigap plans to those under 65, and the only two that do so voluntarily are United American (Plans B and HDF) and Blue Cross Blue Shield of North Dakota (Plan F).

- Ohio: ❌

- Oklahoma: ✅– those under 65 have the same premiums as those who are 65; every carrier must offer at least one plan.

- Oregon: ✅

- Pennsylvania: ✅– carriers are required to offer Medigap to those under 65, and while they aren't required to limit premiums, carriers seem to be doing it on their own. The cost for under 65 Medigap plans is the same as those aging in to Medicare.

- Rhode Island: ⚠️– only Blue Cross Blue Shield of Rhode Island offers Plan A.

- South Carolina: ❌

- South Dakota: ✅– plus, state regulations prohibit Medigap carriers from charging enrollees under 65 more than they charge enrollees who are 75.

- Tennessee: ✅

- Texas: ✅– carriers must offer at least Plan A.

- Utah: ⚠️– carriers don't have to offer Medigap plans to those under 65, and the only one that does is United American. However, only Plan B, and for just under $5,000 per year.

- Vermont: ✅

- Virginia: ⚠️– new legislation will require Medigap carriers to offer at least one GI plan starting in 2021.

- Washington: ⚠️– out of 25 Medigap carriers, only two offer plans to people under age 65 – United American and the Washington State Health Care Authority plan.

- West Virginia: ⚠️– only United American offers Plan A.

- Wisconsin: ✅

- Wyoming: ⚠️– but out of 27 Medigap carriers, only two offer plans to people under age 65 – United American and Liberty National Life.

Medigap pricing for individuals under 65

As you can see, there's a mix of three basic situations:

- The state requires Medigap carriers to offer plans to those under 65

- The state doesn't require Medicare carriers to offer plans to those under 65, but some carriers voluntarily choose to do so

- The state doesn't require Medicare carriers to offer plans to those under 65, and no carriers offer any

In the states that do have Medigap options for those under age 65, the pricing can be very expensive.

Outside of the few states with regulations that limit how much carriers can charge (Hawaii, Kansas, Missouri, etc.) or states with community-rated plans (New York and Connecticut), you're looking at premiums in the $3,000-$35,000 range.

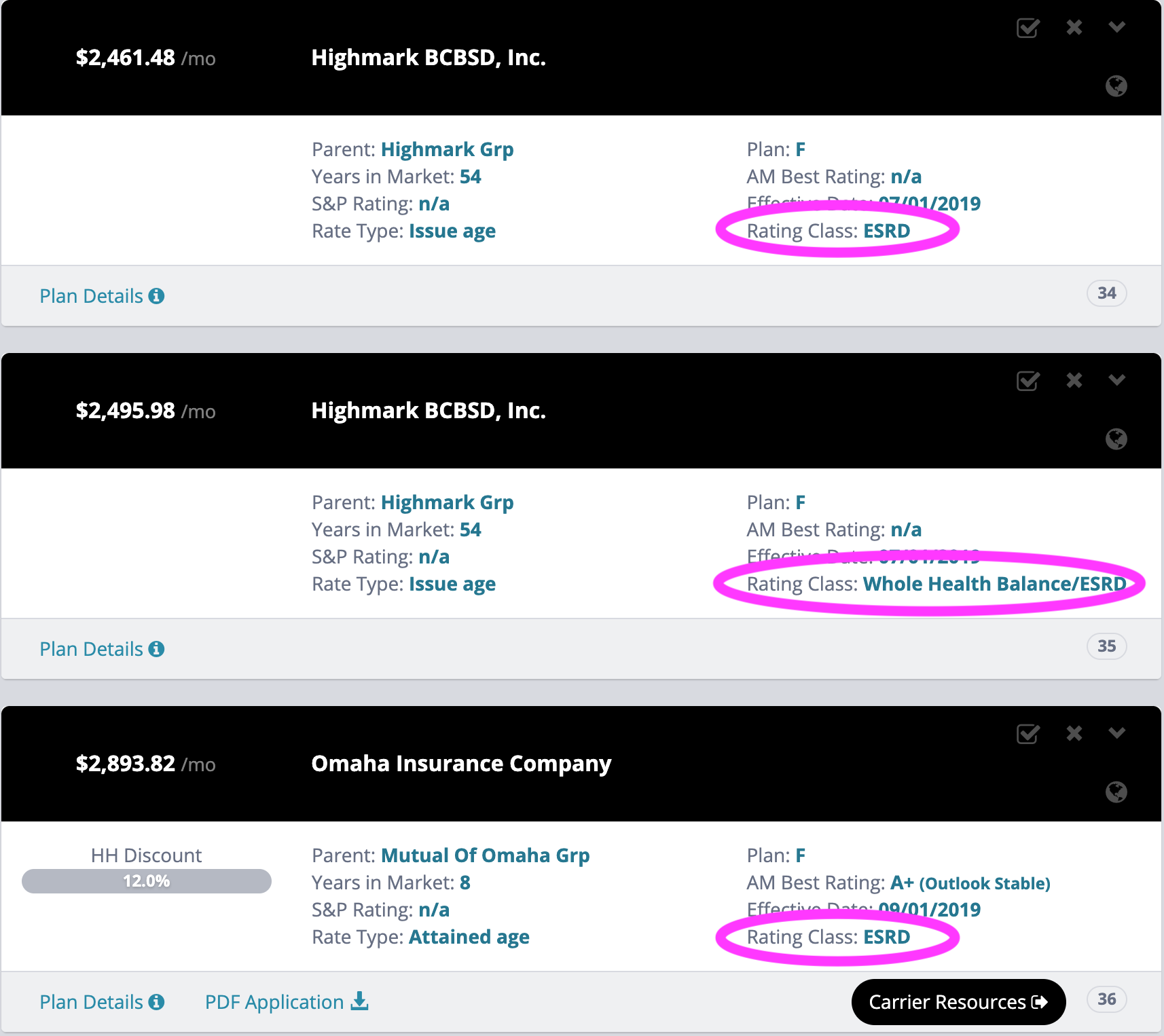

Yes, $35,000 is a real premium figure for those in Delaware who have ESRD:

Rate samples for those with ESRD in Delaware (effective 6-3-20)

You can check plan availability and rates at any time using our Quote Engine. Just put in your zip code and select "64 – Disabled or ESRD" for the age. The pricing is the same whether you're 30 or 64.

A second chance at age 65

In most states, you get a second open enrollment window as you age into Medicare. So in Illinois, for example, your 64-year-old client may be paying $300/mo for a Medigap plan.

But as they turn 65, they get a second opportunity to get any Medigap plan they want, and they pay 65-year-old rates.

So, they could theoretically go from paying $300/mo at age 64 to paying $100/mo at age 65.

Here's a visual of what that'd look like for a client in Illinois:

| Age 62 | Age 63 | Age 64 | Age 65 |

| $226.57 | $226.57 | $226.57 | $94.49 |

Plan G, showing quotes for Cigna under 65 and GSL at 65 in Macon County, IL (pulled 6-3-20)

It's something to look forward to!

Commission for under 65 Medigap plans

As an agent, you want to look at the prices – obviously – but you also want to look at what commission that carrier is offering. A lot of carriers won't pay you anything for under 65 business.

And some carriers will only pay you a low, flat rate around $25. In most cases, you'll get a drastically reduced commission for an under 65 application.

However, some carriers will pay full comp for under 65 business. It depends on the state.

Just check with us on that, because as you can tell, it's all state-specific.

Medicare Advantage Under Age 65

If your client is disabled and under age 65, they can get a Medicare Advantage plan when they become eligible for Medicare.

Here's the official eligibility criteria for MA:

- You have Part A and Part B

- You live in the plan’s service area

- You’re a U.S. citizen, U.S. national, or lawfully present in the U.S.

- You don’t have End-Stage Renal Disease (ESRD)

As explained earlier in this article, your client is automatically enrolled in Medicare Parts A and B after 24 months of getting disability benefits from Social Security or the RRB.

Starting in 2021, people with ESRD will be able to join Medicare Advantage Plans without restrictions. But until then, those with ESRD can only join an MA plan if they fall into one of these circumstances outlined by CMS:

- If you’re already in a Medicare Advantage Plan when you develop ESRD, you can stay in your plan or you may be able to join another Medicare Advantage Plan offered by the same company.

- If you’re in a Medicare Advantage Plan, and the plan leaves Medicare or no longer provides coverage in your area, you have a one-time right to join another Medicare Advantage Plan.

- If you have an employer or union health plan or other health coverage through a company that offers one or more Medicare Advantage Plan(s), you may be able to join one of that company’s Medicare Advantage Plans.

- If you’re medically determined to no longer have ESRD (for example, you’ve had a successful kidney transplant), you may be able to join a Medicare Advantage Plan.

- You may be able to join a Medicare Special Needs Plan (SNP) that covers people with ESRD if one is available in your area.

The Medicare MSA Under Age 65

The Medicare MSA is a type of Medicare Advantage plan, so the same eligibility criteria apply. That means your disabled clients under age 65 would qualify for the MSA unless they have ESRD.

MA vs. Med Supps for Under Age 65

In states where there aren't Medicare Supplement options for people under age 65, you need to go down the Medicare Advantage route.

Take a look at what the options are in your county and move forward just like you would with someone age 65+.

In any case, don't discount MA plans. It could be the best option for your under 65 disabled clients.

Be a Full-Service Agent

Michael Sams, Director of Sales Training and Development, explains that he does a full-blown CNA with every client that's eligible for Medicare – regardless of age.

Michael Sams, Director of Sales Training and Development, explains that he does a full-blown CNA with every client that's eligible for Medicare – regardless of age.

For those who are disabled and under age 65, the products that come up most often are life insurance and annuities (typically from rolling over a retirement account).

In any case, you want to go through all of those fact-finding questions to make sure you're fully serving your client. Don't assume they have no money or can't afford insurance protection without asking.

Finally, Michael explains that even if you make no commission – perhaps the only option for them is a Medigap plan that offers no comp for under age 65 – there's still fruit to be had.

"Referrals!" he says. "That person will tell others that I helped them, and the word travels."

Conclusion

In general, to qualify for Medicare benefits, your client must be getting disability benefits from Social Security or the RRB for 24 months.

At that point, it's up to you to determine the possible options: Medicare Supplement, Medicare Advantage, or the Medicare MSA.

Your options are largely determined by which state you're in, so reference our state availability list earlier in this article to help you.

In states where Medigap plans are available, prepare to see some staggering premiums – in most states, if you're under age 65 and are disabled, carriers treat you like you're 99.

If the premiums are $5,000+, consider pivoting to a Medicare Advantage plan or the Medicare MSA, which may offer lower out-of-pocket costs for the year, even if your client hits their out-of-pocket maximum.

If you have any questions about a specific client or case you're dealing with, reach out! Give us a call anytime at 888-780-7676 or start a chat here on our website.

What's your experience with helping disabled clients under 65 in your state?

Comments