If you’re selling Med Supps like hotcakes but you haven’t taken a look at annuities, you’re missing out on a big slice of the insurance pie (are you hungry yet?).

Annuities are really easy to bring up to your senior clients, because at the end of the day, we all want the same thing.

- We want safety.

- We want a good rate of return on our investments.

- And by golly, we want an income that will outlive us.

If you do a full Client Needs Assessment on all of your clients, you’re uncovering that your clients aren’t always happy with their current rate of return.

This is the perfect opportunity to introduce fixed indexed annuities. Did we mention that you receive an average of 2-4% commission on them? If you aren’t already offering annuities to your clients, you're leaving a huge chunk of business on the table.

Need a brush-up on annuities?

OK, let’s polish your memory.

People need balance.

Balance between reward and risk, nest egg preservation and growth, vanilla and chocolate ice cream.... OK, just kidding about that last one.

But seriously, no one knows what the future holds, and that’s why indexed annuities are perfect for retirement savers. They’re also perfect for those who have a large lump of cash sitting around that’s not earning any interest.

It doesn’t matter what happens in the stock market — an indexed annuity won’t lose value.

In 2008-2009, Americans lost a ton of retirement money because of the stock market. Those that had indexed annuities didn’t lose anything.

So, what exactly are annuities?

Annuities are a contract between your client and the insurance carrier. They can pay for the annuity either:

- With a lump sum, or

- With multiple payments over time.

In return, the insurance company promises to pay the client money from the annuity in a single or series of payments.

Like many other long-term financial products, annuities have a surrender fee for early withdrawal. The terms depend on the individual contract.

There are two categories of annuities:

- Fixed

- Variable

New Horizons doesn’t offer variable annuities because of the risk involved that is not advantageous to our senior market.

With fixed annuities, the insurance company assumes the risk, not the client.

An indexed annuity is a type of fixed annuity. These have a distinct way of calculating annual interest using a formula based on performance changes of a:

- Stock,

- Bond, or

- Commodity index.

The index is used as an external benchmark — the client doesn’t actually invest in it.

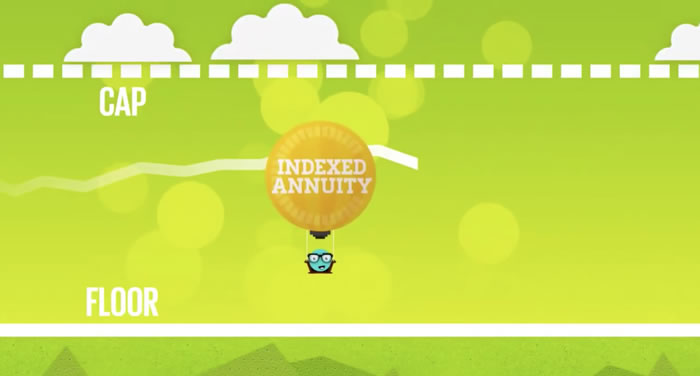

While the interest earned depends on the feature of the individual contract, indexed annuities generally have an interest rate floor, a participation rate, and a cap that determine the amount of interest the client will earn.

The interest earned always remains somewhere between the floor and the cap. It doesn’t rise above the cap, even if the index happens to go higher. BUT, it never falls below zero, even if the index takes a hard fall. The value of the money invested will never decline, but it can definitely increase.

Once interest is credited, it also can never be lost due to interest rate adjustments or negative market fluctuations. It may even compound, which means more potential growth than other kinds of annuities or regular savings plans.

Like all annuities, the indexed type offers tax-deferred growth.

The process of choosing an index annuity can give your clients peace of mind. Let them know that these products are backed by the world’s largest, most reputable insurance companies.

Now that you know the basics about indexed annuities, what are you waiting for? If you have more questions, give us a call. Otherwise, check out the annuities we offer, bring up this important conversation with your clients, and starting make more (way more) commissions!

Comments