By Jeff Sams, John Hockaday, and Luke Hockaday

Whether you want to get into Med Supp sales or you're considering getting your non-resident license in other states, you want your efforts to really count.

In addition, COVID-19 has forced agents across the country to service clients from home. Now that you know how to do everything remotely, why not expand your Med Supp business into new states?

Medicare Supplements are available in every state, but some are arguably "better" to sell in than others. We're taking a look of all the important factors, including Medicare Advantage penetration, Med Supp enrollment numbers, the cost to get a non-resident license, street level commissions by state, and more.

Here's what we're covering, and you can jump ahead to any section:

- There's No "Magic" State

- Medigap Enrollment By State

- Medicare Advantage Penetration By State

- Non-Resident License Fees By State

- Street Level Commission By State

- States With Best and Worst Med Supp Rates

- A Note on Indiana

- A Note on the Birthday, or Anniversary, Rule

- Best (and Worst) States for Med Supp Sales

There's No "Magic" State

Before we get into all the comparisons and analysis, I think it's important to say that there's no one magic state to start selling in where you're guaranteed to make a killing.

There are certain states that stand out to us, but it often comes down to the county. Illinois might be a great state for Medicare Supplement sales, but it's definitely easier to sell in central IL than Chicago!

Related: Is It Hard to Sell Medicare Supplements?

Rural areas tend to have the fewest Medicare Advantage options, which typically aren't that attractive anyway. In these areas, Medicare Supplements are usually a no-brainer, which makes selling them... well, easy.

Even if a state doesn't necessarily make our list of suggestions, don't discount it. There are almost definitely going to be counties in that state where there's a need for Medicare Supplement agents.

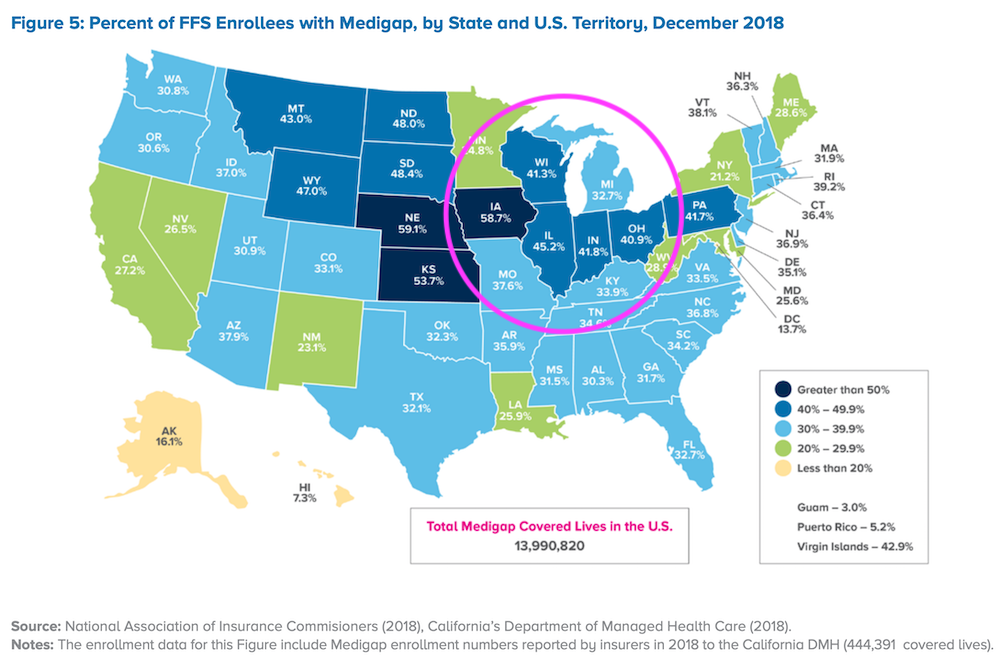

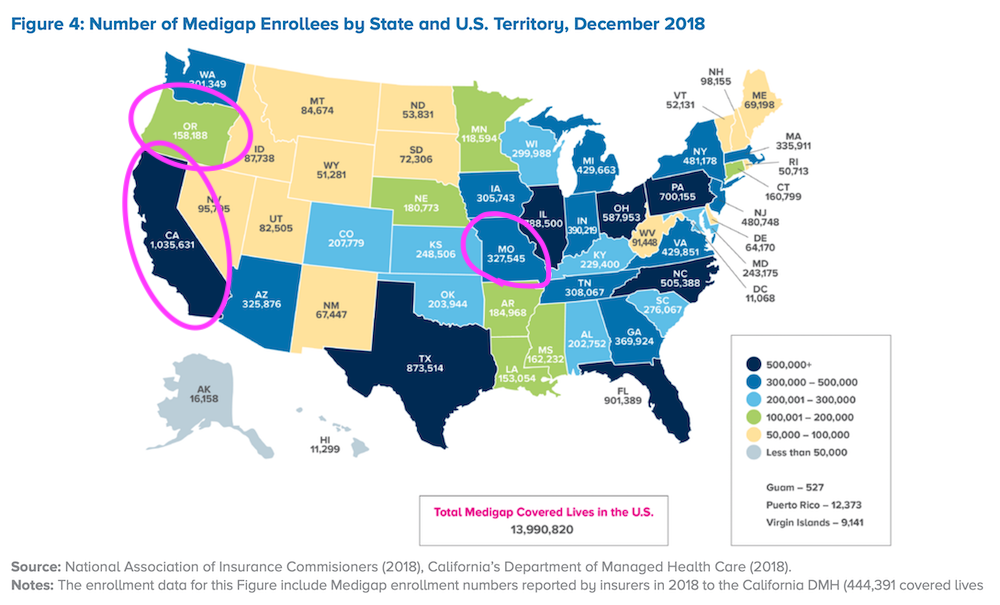

Medigap Enrollment By State

When considering which states you might want to expand into, looking at Medigap enrollment numbers can be really helpful. The data in this section is from the AHIP State of Medigap 2020 report.

The more populated a state is, the more Medigap enrollments it will have, but it still gives you a good idea of the opportunity.

The midwest is a particularly great area for Medigap enrollments, including states like:

- Illinois

- Indiana

- Iowa

- Missouri

- Ohio

- Wisconsin

- Michigan

Other states that stand out include North Carolina, Texas, Georgia, Pennsylvania, and Virginia.

Medigap Enrollments by State Table

| Alabama: 202,752 | Indiana: 390,219 | Nevada: 95,795 | South Dakota: 72,306 |

| Alaska: 16,158 | Iowa: 305,743 | New Hampshire: 95,155 | Tennessee: 308,067 |

| Arizona: 325,876 | Kansas: 248,506 | New Jersey: 480,748 | Texas: 873,514 |

| Arkansas: 184,968 | Kentucky: 229,400 | New Mexico: 67,447 | Utah: 82,505 |

| California: 591,240 | Louisiana: 153,054 | New York: 481,178 | Vermont: 52,131 |

| Colorado: 207,779 | Maine: 69,198 | North Carolina: 505,388 | Virgin Islands: 9,141 |

| Connecticut: 160,799 | Maryland: 243,175 | North Dakota: 53,831 | Virginia: 429,851 |

| Delaware: 64,170 | Massachusetts: 335,911* | Ohio: 587,953 | Washington: 301,349 |

| District of Columbia: 11,068 | Michigan: 429,663 | Oklahoma: 203,944 | West Virginia: 91,448 |

| Florida: 901,389 | Minnesota: 118,594* | Oregon: 158,188 | Wisconsin: 299,988* |

| Georgia: 369,924 | Mississippi: 162,232 | Pennsylvania: 700,155 | Wyoming: 51,281 |

| Hawaii: 11,299 | Missouri: 327,545 | Puerto Rico: 12,373 | |

| Idaho: 87,738 | Montana: 84,674 | Rhode Island: 50,713 | |

| Illinois: 788,500 | Nebraska: 180,773 | South Carolina: 276,067 |

*Waivered state: Three states (Massachusetts, Minnesota, and Wisconsin) offer standardized Medigap plans but are exempt from the OBRA 1990 standardized plan provisions (and subsequent revisions under the MMA or MIPPA). Standardized plans may therefore be changed by waivered states without federal approval. Individuals who purchase Medigap plans in one of these three states may keep their plans if they move to other states.

While a state like Florida has the highest number of Medigap enrollments in the country, they also have the highest percentage of Medicare Advantage enrollments (more on this in the next section).

Florida may seem like one of the best states to expand into, but the MA competition is fierce.

The same goes for a state like California. It has over half a million Medigap enrollees, but nearly 2.5 million Medicare Advantage enrollees (KFF).

The Medicare Advantage options in these states are very competitive – in many counties, there's no way a Medicare Supplement can compete.

Speaking of Medicare Advantage...

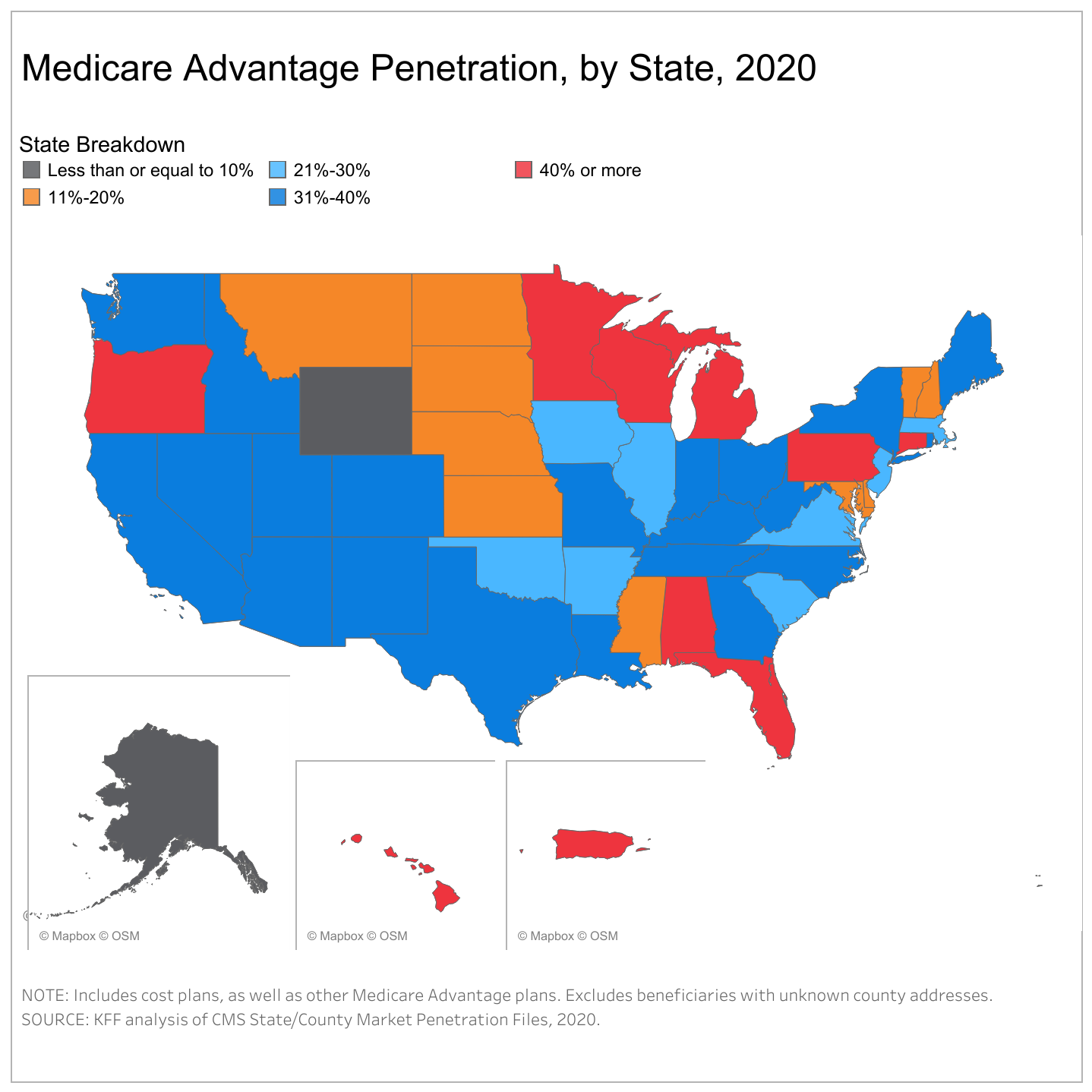

Medicare Advantage Penetration by State

The Medicare Enrollment Dashboard from CMS offers a clear, current picture of what Medicare products are being sold where.

We can look at Original Medicare vs. Medicare Advantage enrollments at a national, state, or county level.

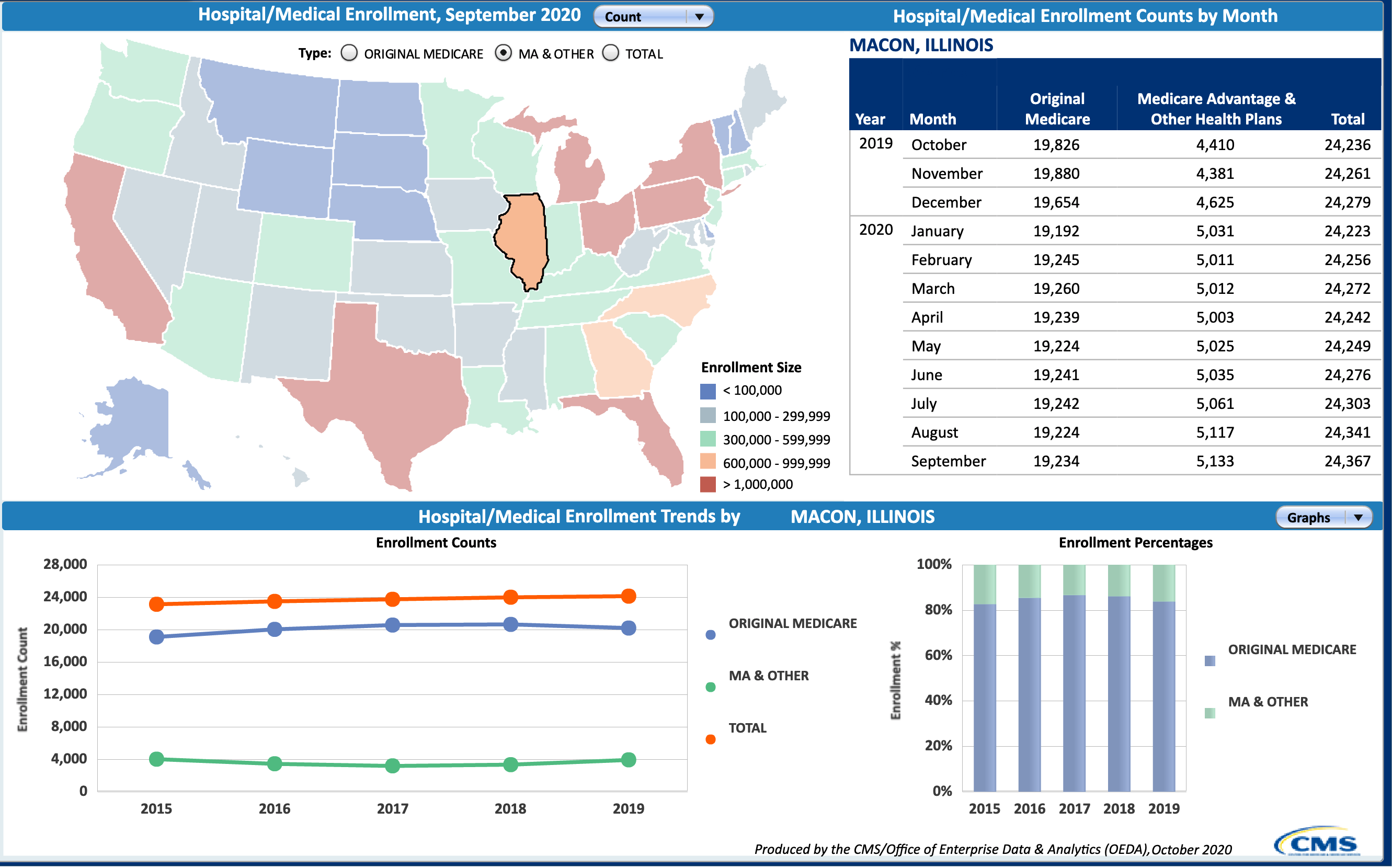

If you've decided you want to get a non-resident license in another state, consider taking a look at the counties there with this dashboard. You may decide to select a few zip codes to focus on, because there's less MA penetration.

For example, in Macon County, Illinois, a vast majority of Medicare eligibles chose Original Medicare over Medicare Advantage. If you look at the chart below, you can see the enrollment numbers in the top right, which can help you spot trends. Ask questions like:

- Are the Medicare Advantage numbers growing each month at the same rate as Original Medicare?

- Are Original Medicare numbers going down over time?

- Can I assume, based on these numbers, that people are dropping Original Medicare in favor of Medicare Advantage?

- What's the opportunity here?

Interested in Medicare Advantage sales training? Get free access to our Medicare Advantage video training series by clicking the image below:

The enrollment percentages chart in the bottom right also gives you a quick look at what the MA penetration is. With over 80% of folks choosing Original Medicare, that signals to me that Macon County is a great county to sell Med Supps. (And it is!)

Macon County, IL Medicare Enrollment Numbers

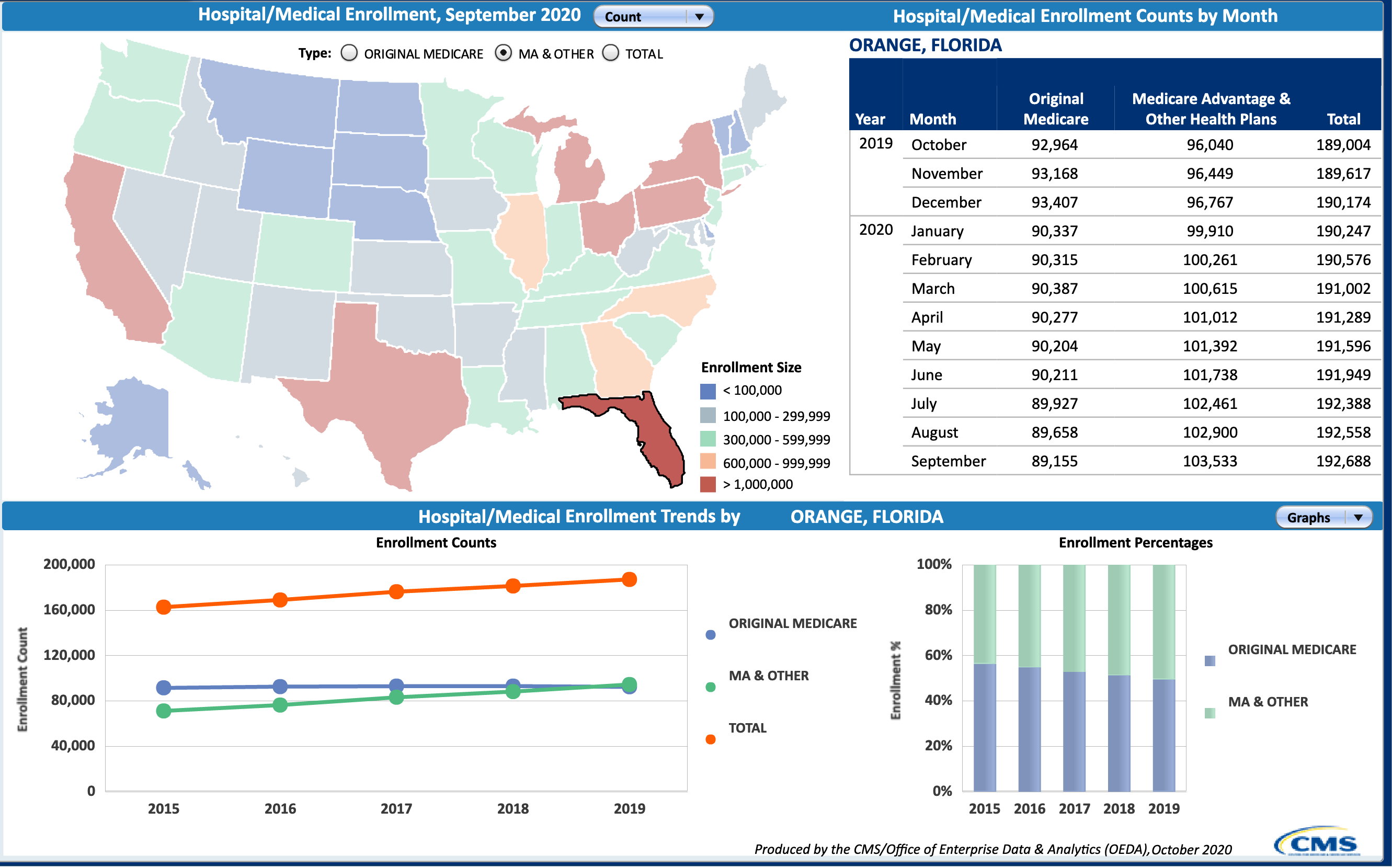

On the other hand, when we go to a place like Orange County, Florida, we see the opposite story. MA penetration is high here, and Original Medicare numbers are going down month-over-month.

Orange County, FL Medicare Enrollment Numbers

If an area has a heavy MA penetration, it might not be the best place to sell Medicare Supplements.

There's no hard and fast rule, but I'd say any county where MA penetration is under 25-30% is a good one to focus on.

The higher the MA penetration, the "louder" the Medicare Advantage advertising will be. It's simply harder to break through the noise.

Going down to the county level be very helpful, because rural areas have fewer options, while metro areas are typically heavier in MA.

Considering statewide enrollment numbers alone, the following states have heavy MA penetration:

- Oregon

- Florida

- Minnesota

- Wisconsin

- Michigan

- Pennsylvania

- Hawaii

- Alabama

Based on the heavier MA penetration, these may be the worst states to sell Medicare Supplements. Again, not impossible by any means – perhaps just a little more challenging.

On the other hand, states like Wyoming, Montana, North Dakota, South Dakota, Nebraska, Kansas, Mississippi, Maryland, Delaware, Vermont, and New Hampshire have really low MA penetration.

These may be some of the best states to consider expanding into if you're concerned about the MA competition.

Non-Resident License Fees By State

If you want to expand and serve senior clients in multiple states, you'll need to get your non-resident license. Costs vary by state, and it can be a hassle to compare them all. You have to check each state individually on the NIPR website.

We consolidated all of the information in one place for you. Based on our research, the states with the lowest cost non-resident licenses include:

- Michigan

- New Mexico

- South Carolina

- South Dakota

- Iowa

- West Virginia

- Texas

- Florida

The most expensive non-resident licenses come from:

- Puerto Rico

- Virgin Islands

- Hawaii

- Massachusetts

To see what all states charge, we created a table that gives you a birds-eye view. Please note that in addition to the fees outlined below, there is a $6.18 transaction fee (NIPR) when applying for a Non-Resident license.

Also, some states charge per Line of Authority. Medicare Supplements are Health, but most agents get Life & Health. We're only including the cost for a non-resident Health license. If you need multiple Lines of Authority, we've included an asterisk next to the states that have extra fees for additional lines. You can also check the fee structure for your state on the NIPR website.

| Alabama: $80 | Indiana: $90+** | Nevada: $185 | South Dakota: $30 |

| Alaska: $75 | Iowa: $50 | New Hampshire: $210 | Tennessee: $50-$800** |

| Arizona: $120 | Kansas: $80 | New Jersey: $170 | Texas: $50 |

| Arkansas: $70 | Kentucky: $50* | New Mexico: $30 | Utah: $75 |

| California: $188 | Louisiana: $75 | New York: $40-$1,682** | Vermont: $30+** |

| Colorado: $71* | Maine: $55 | North Carolina: $44* | Virgin Islands: $700 |

| Connecticut: $140 | Maryland: $54 | North Dakota: $100 | Virginia: $15* |

| Delaware: $100 | Massachusetts: $225 | Ohio: $10* | Washington: $60 |

| District of Columbia: $100* | Michigan: $10 | Oklahoma: $100 | West Virginia: $50 |

| Florida: $50* | Minnesota: $75* | Oregon: $75 | Wisconsin: $75* |

| Georgia: $120* | Mississippi: $101 | Pennsylvania: $110 | Wyoming: $150 |

| Hawaii: $225-$300 | Missouri: $100 | Puerto Rico: $1,682 | |

| Idaho: $80 | Montana: $100 | Rhode Island: $130 | |

| Illinois: $250 | Nebraska: $50 | South Carolina: $25 |

*Higher fees apply for multiple Lines of Authority

**Retaliatory fees may apply. Retaliatory fees are fees imposed by a Department of Insurance on another state's insurance professionals.

Hopefully, this chart helps you quickly calculate the cost to expand your Med Supp business into new states.

Street Level Commission By State

While every carrier is different, we took a look at our most popular national carrier to compare Medicare Supplement commission rates by state. Street level commission is very similar across the board, but some states do stand out slightly when compared to the rest.

For example, Florida agents get 2 points less than the comp paid in most other states. Michigan agents get full comp for the first 3 years compared to the typical 6, but the comp is 7 points higher. Agents in Ohio and Indiana get no comp after the first 6-7 years.

Our contracting department says while there are some subtle differences between states, the commission ultimately seems to average out.

Each of these comp charts is for Open Enrollment and Underwritten business for clients age 65+. This is commission for all marketed plans except Plan N – some states pay more on Plan N, but not all.

Full Comp Years 1-6

| Policy Years 1-6 | Policy Years 7+ | |

| Alabama | 22% | 2.5% |

| Arizona | 22% | 2.5% |

| Arkansas | -- | -- |

| California | 22% | 2.5% |

| Colorado | 22% | 2.5% |

| Connecticut | -- | -- |

| Delaware | 21% | 3% |

| District of Columbia | -- | -- |

| Florida | 20% | 2.25% |

| Georgia | 22% | 2.5% |

| Hawaii | -- | -- |

| Idaho | 22% | 2.5% |

| Illinois | 22% | 2.5% |

| Indiana | 22% | 0% |

| Iowa | 22% | 2.5% |

| Kansas | 22% | 2.5% |

| Kentucky | 22% | 2.5% |

| Louisiana | 22% | 2.5% |

| Maine | -- | -- |

| Maryland | 22% | 2.5% |

| Massachusetts | -- | -- |

| Minnesota | 22% | 2.5% |

| Mississippi | 22% | 2.5% |

| Missouri | 22% | 2.5% |

| Montana | 22% | 2.5% |

| Nebraska | 22% | 2.5% |

| Nevada | 22% | 2.5% |

| New Hampshire | 22% | 2.5% |

| New Jersey | 22% | 2.5% |

| New Mexico | 22% | 2.5% |

| New York | -- | -- |

| North Carolina | 22% | 2.5% |

| North Dakota | 22% | 2.5% |

| Oklahoma | 22% | 2.5% |

| Oregon | 22% | 2.5% |

| Pennsylvania | 22% | 2.5% |

| Rhode Island | 22% | 2.5% |

| South Carolina | 22% | 2.5% |

| South Dakota | 22% | 2.5% |

| Tennessee | 22% | 2.5% |

| Utah | 22% | 2.5% |

| Vermont | 22% | 2.5% |

| Virginia | 22% | 2.5% |

| Washington | -- | -- |

| West Virginia | 22% | 2.5% |

| Wisconsin | 22% | 3% |

| Wyoming | 22% | 2.5% |

Full Comp Years 1-3

| Policy Years 1-3 | Policy Years 4+ | |

| Michigan | 29% | 4.5% |

Full Comp Years 1-7

| Policy Years 1-7 | Policy Years 8+ | |

| Ohio | 20% | 0% |

| Texas | 22% | 2.5% |

Note: This carrier does not offer a Medicare Supplement product in Arkansas, Connecticut, D.C, Hawaii, Maine, Massachusetts, New York, or Washington.

Another popular carrier we checked has a similar commission structure as this one, but there are some subtle differences:

- Georgia, Arkansas, and Arizona pay 2 points less than the rest.

- Oregon and Florida pays 5 points less than the rest (and no comp after year 6).

- Indiana pays 1 point more but has no comp after year 6.

- Michigan has a high comp in years 1-3, it goes down in years 4-6, down again in years 7-10, and then nothing after year 10.

- Because of the anniversary rule, Missouri's comp is significantly lower than the rest of the states (about half!).

While, for the most part, the commission is comparable between states, there can be some subtle differences that might sway you to focus on one state over another.

States With Best and Worst Med Supp Rates

When rates are good, there's going to be more interest in Medicare Supplements.

Compare Illinois to Florida, for example. Here in Illinois, you can be 65 and buy a good Plan G for $100. In Florida, it's double that for the same thing.

Medicare Supplements are sold everywhere, but you have to understand the market. Medicare Advantage is expanding like wildfire, and in states like Florida, consumers are better off going that way.

While here in the midwest, particularly in more rural areas, Medicare Supplements are the best option.

According to Howmuch.net, the 10 states with the highest Med Supp rates are:

- Massachusetts

- Nevada

- Louisiana

- New Jersey

- Maryland

- Connecticut

- Texas

- Alaska

- Florida

- California

You also have to remember rates vary based on zip code. Rural counties have lower Med Supp premiums than metro ones. Take Illinois, for example. Here in Decatur, you can buy a G for $95 a month. Head up to Chicago, and you're paying $110 for the same thing.

This is a trend you'll see all across the country. A Plan G in Lockhart, Texas is $95, and the same thing in Dallas is $107. Gainesville, Georgia has a Plan G for $110, while 60 miles away, Atlanta has it for $120.

If you're thinking about getting your non-resident license in other states, I'd do some analysis on the rates in the counties you want to focus on. Use our quote engine, and take a look at that county on the Medicare Enrollment Dashboard.

A Note on Indiana

A Note on Indiana

Indiana is a critical state in the Medicare Supplement world. It's a state that every carrier wants to do well in – agents put their best foot forward there. None of us have been able to figure out why carriers battle over Indiana so hard!

Mutual of Omaha may have started it, and they've always fought tooth and nail to have the best rate there. You can get some incredible rates in Indiana, which makes it a great state to sell Medicare Supplements.

A Note on the Birthday, or Anniversary, Rule

Missouri, California, and Oregon have the "birthday" or anniversary rule.

The anniversary rule offers Med Supp enrollees a 30-day window following their birthday each year when they can switch to another plan without going through underwriting.

Some agents think Missouri, California, and Oregon are the best states to sell Med Supps in because of this rule. While there may some merit to that, there's always a trade-off.

What happens is those states end up having higher premiums for everyone. They have to cover the cost of the higher claims since there's no underwriting. Commissions are also typically lower in these states.

Some people will benefit from that rule, but on the other hand, some people are paying more than they should be paying for coverage.

It's just some food for thought.

Best (and Worst) States for Med Supp Sales

States with low Medicare Advantage penetration, high Medicare Supplement enrollment, competitive Med Supp rates, reasonable non-res licensing fees, and good commissions are great states for selling Medicare Supplements.

The best states to sell Medicare Supplements are Indiana, Illinois, Iowa, South Dakota, Kansas, New Mexico, Michigan, Arizona, and Texas.

States with high MA penetration and expensive Med Supp premiums fall to the bottom of the list when choosing which states to focus on.

Using our analysis, the worst states to sell Medicare Supplements are California, Florida, Massachusetts, New York, Pennsylvania, and Alabama. Other websites might tell you these are some of the best, but when you consider the high premiums and preference for Medicare Advantage, they're not our first choice.

Conclusion

Regardless of our recommendations, you can be successful selling Medicare Supplements no matter where you live! With a focus on education and serving your clients to the best of your ability, you'll do great.

We hope this helps you determine the best states to consider when expanding your Medicare Supplement business. Good selling!

Comments