Getting started with life insurance sales can be intimidating at first – there are several different kinds, and dozens of carriers to choose from.

And even then, once you become familiar with the product knowledge, you need to learn how to properly execute the sale. Selling life insurance in the senior market doesn't have to be difficult, and we'll show you why.

By the time you're done reading, you're going to be ready to start selling life insurance to the senior market.

Jump ahead to any section:

- Life Insurance Types

- Why Seniors Might Need Life Insurance

- Starting the Life Insurance Conversation

- Life Insurance Policy Reviews

- Life Insurance Script for Practicing Your Presentation

- 4 Real Life Insurance Sales Examples

- Smokers vs. Non-Smokers

- Training, E/O Insurance, and Contracting

- Writing Personal Notes to Underwriters

- How to Market Life Insurance to Seniors

- Get Started with New Horizons

Life Insurance Types

If you're already familiar with life insurance, you know how many different types there are. It can feel complicated at first, but when you break it down, it's really simple!

1. Term Life Insurance

Buying a term life insurance policy is the most affordable way to carry a large death benefit.

Term life insurance is typically used by clients interested in covering debt or replacing income in the event of premature death. Term life is for a specific term ranging from 5-30 years.

In the senior market, we don't really sell term very often, because it just doesn't fit the needs of our older clientele. Unless your senior client has just taken on a mortgage or something of that nature, you won't really be dealing with term life insurance.

However, if you're in the senior market and are looking to expand to a younger group, this is an excellent product to start with as it's needed, and the commission can't be beat.

2. Final Expense Life Insurance

Final expense policies are the bread and butter of many senior market insurance agents. Some agents sell it exclusively, but I'd say the vast majority offer it as a key ancillary product to boost their Med Supp sales.

Final expense is used to cover funeral costs and any final bills associated with the end of life. These are typically the policies with the lowest death benefits.

There are 4 different types of final expense policies: level, graded, modified, and GI.

Level

Level plans are the least expensive and provide an immediate death benefit.

Graded and Modified

Graded and Modified final expense plans will pay a portion of the death benefit or offer a return of premium + interest during the first 2 years. After 2 years, the client will qualify for the full death benefit.

GI

A guaranteed issue final expense plan has no health questions.

Everyone within the age parameters qualifies for this plan. There is a 2-year waiting period for the client to qualify for the full death benefit. If the client dies within the first 2 years, the beneficiary would receive return of premium + interest.

If you’d like to dig in and learn more about final expense policies, read Final Expense Insurance: Level, Graded, Modified, and GI (2nd Edition).

3. Whole Life Insurance

Whole life insurance is a type of permanent insurance that also builds cash value. It’s known to be one of the most expensive types of life insurance.

Whole life participates – its dividends buy more insurance that in turn go back into the policy. This is called paid-up additions.

We can get into the weeds pretty quickly, but all you really need to know about whole life is that it accumulates cash value and is more expensive than other types of permanent life insurance.

4. Universal Life Insurance

Universal Life offers a permanent solution for a client with possible flexibility of premium and cash accumulation potential.

5. Life Insurance with a Long-Term Care Rider

A permanent life insurance policy with the LTC rider provides a single solution to help meet critical needs that clients often face.

Those needs include:

- Immediate funds in case of death

- Monthly access, if needed, to a portion of the policy’s death benefit to help pay for long-term care expenses

This is the most complex policy, and it’s often the most expensive. However, the commissions on these policies are greater than most.

Check out this case study:

Why Seniors Might Need Life Insurance

We've found that the senior individual might need life insurance for a few reasons:

- Leave a legacy

- Cover final expenses and burial costs

- Income replacement for those that are dependent on current income

- Cover outstanding debt

A potential fifth reason revolves around the potential long-term care solution. If your client needs a solution for expensive LTC costs, the Life w/ LTC rider is a great hybrid option that ensures someone will be paid.

1. Leave a legacy

Many individuals like the idea of leaving money for their kids and grandkids.

There are different permanent life insurance policies, and sometimes, your savings can build cash value and offer a better death benefit. This means that it generally makes more financial sense to leave a legacy for your children through a life insurance policy versus just savings in the bank.

Additionally, you can use life insurance to leave a donation to a charity or a church.

2. Cover final expenses and burial costs

Many funerals with modest arrangements cost more than $10,000. These prices also vary depending on which state you live in, and they’ve been rising steadily over time.

There are other end-of-life costs to consider, such as medical bills, any credit card debt, legal expenses like probate, and so on.

The beauty of a final expense policy is once the insurance company confirms your death, they immediately send your death benefit to your beneficiary. That person can choose how to spend the money, so if they need $10,000 for your funeral, and $2,000 for your credit card debt, they can take care of that right away.

3. Income replacement for those that are dependent on current income

Many seniors rely on their spouse's pension or Social Security checks – without it, they wouldn't be able to keep their current standard of living.

A life insurance policy can provide that income replacement if they lose a loved one that they're still dependent on.

4. Cover outstanding debt

In a perfect world, our retirement years would mark an era of no debt, but unfortunately, that's not the case. New 2018 data from the Survey of Consumer Finances found that around 60% of households that are headed by an adult 65+ are in debt. That has been rapidly increasing since 1992, when it was around 41%.

That's a lot of seniors that are in debt, and if someone else is on the hook for it, a life insurance policy can make sure they aren't stuck with it.

5. Utilize the LTC benefits

Many individuals prefer the Life w/ LTC hybrid insurance product over traditional Long-Term Care Insurance, because you know you’re going to use it. Your loved ones will get the death benefit when you pass, but if you do end up in a nursing home or with the need for extra care, you can pull a percentage of your death benefit out early to help.

That's just part of it – traditional LTCi is very expensive, most carriers have pulled out of the market and don't offer it, and those that have it experience rate hikes. Because of that, Life w/ LTC can be a real solution for clients who don't have a plan if LTC costs arise.

Starting the Life Insurance Conversation

If you've been reading our stuff for a while, you know that discovering the need is the key to success.

There's no better way to serve your clients than to offer personalized solutions based on what they actually need.

So all of those needs we just went over? Those are going to come in handy.

To start the life insurance conversation, you're going to begin with the Client Needs Assessment (CNA).

Use the CNA!

Questions 7 and 8 are going to aid you with bringing up the conversation.

Question #7: Do you currently carry any life insurance?

Once you ask this question, you're going to roll through the follow-up questions:

- What's the death benefit?

- What's your premium?

- What's the cash value?

- What purpose does it serve?

Write down the responses on your CNA as you go.

Question #8: Have you made any arrangements to take care of final expenses?

You can tag on a final expense policy to a Medicare Supplement with ease. In any case, if they don’t have final expense insurance or insurance that will cover these costs, you can build the need by asking this question.

You should also inform your client that the average cost for a funeral is around $15,000. If they have made arrangements, but it’s only for $5,000, you can help by adding on the appropriate amount.

Life Insurance Policy Reviews

The whole purpose of doing a life insurance policy review is to ensure your client's needs are covered. If they choose not to take your advice, that's their prerogative, but at the very least, you've done your job by educating them.

If you'd like to see the flow of the CNA questions in action, watch this roleplay scenario of a life insurance policy review:

You want to obtain an annual statement or an in-force illustration from the client if you can, and then you can send it to Kirk Sarff to review. Our office staff here is very knowledgeable about the options and carriers, and we can help you better your client's situation.

Just like a regular annual policy review, we do suggest doing these about once a year.

Read more about life insurance reviews:

- How to Do a Life Insurance Policy Review (A Shortcut and Real-Life Examples Included)

- [Roleplay] How to Offer a Life Insurance Review to Existing Clients

Life Insurance Script for Practicing Your Presentation

Seeing a script can help you plan for the face-to-face presentation with a client or prospect, so use this script as a guide. The bits in italics are commentary, and the other bits are what you'd say to that client.

The two general situations will be that your client already has life insurance or that they don’t.

If your client already has life insurance

Gather the information about the policy.

There are four main reasons to carry life insurance. Those are:

- to replace your income,

- to cover your final expenses,

- to leave a legacy for your family, or

- to cover any outstanding debt.

Which of these four areas is the reason you carry life insurance?

Does the benefit they have match the need? If yes, commend them for filling the need adequately. If not, make a recommendation for enhancing the coverage.

Filling the Final Expense need when current benefit is not enough

The average cost for standard selections in the state of Illinois is over $16,000.

Adjust this number to match your state.

I would like to recommend you to have some additional life insurance so your family does not have to pay that balance.

*Give at least two, preferably three, options*

Client has a policy with cash value

You’ve had this policy for quite some time, and you’ve accumulated a good chunk of change called cash value.

These older policies were built on projections. Twenty years ago, interest rates were much better than they are today. Those policies were built based off of those interest rates, believing that those interest rates were going to remain consistent. The policy was supposed to perform based on those rates.

We know that the interest rates today are much, much lower than they once were.

Those older policies did not perform the way they were projected.

Because your policy is sometimes going backwards – or losing value – we can take the cash you’ve accumulated in this policy and transfer it to a new one. It’s a non-taxable event, and we can improve your situation.

We can basically put this cash accumulation into a new policy that will stop the bleeding.

If your client has no life insurance

I always recommend my clients to have some type of final expense coverage.

The average cost for standard selections in the state of Illinois is over $16,000. That’s not something we’re going to recommend you leave to your family.

Yes, your family might inherit some money, but we don’t want them to have to sell off the house so they can pay for the funeral.

We have a way to take care of that. Let me show you some options.

Filling Debt, Legacy, or Income Replacement Need

How much money do you feel you need to replace your income / leave to your family / cover your outstanding debts?

Call Kirk in our office for a quote. You’ll want to tell Kirk the benefit needed, birthday of client, medications the client takes, and if the client is tobacco or non-tobacco.

4 Real Life Insurance Sales Examples

Seeing client needs in real life and watching how an agent addresses them is one of the best ways to learn. That's why we've gathered up some of our most popular "Case of the Week" articles and compiled them here for you.

As you can see, the Life w/ LTC option is not to be overlooked!

Life Insurance Sale #1: Life w/ LTC to 59-year-old Male

The client is a 59-year-old male, and the product sold was AIG’s Secure Lifetime GUL3 with Accelerated Access Solution rider. The client had a need for life insurance, and he also didn't have a plan for potential long-term care costs.

For this particular case, the face amount was $250,000, and the monthly LTC benefit was $10,000. Keep in mind that this is an indemnity model, so the client has control of the money.

The annual premium ended up being $4,258, and the client is also putting in a $15,000 lump for year one.

This is not a “use it or lose it” type of policy. You can give your clients some faith in the product by letting them know that benefits will be paid. Those benefits will be paid via the rider acceleration or the beneficiaries at death (or both).

Read the full case study here.

Life Insurance Sale #2: Life w/ LTC to a Younger Couple

By going through the Client Needs Assessment, one of our agents was able to learn that her prospects, a husband and wife, have concerns about long-term care. They currently have family in a nursing home.

She also learned that they are able to budget $500 per month ($250 each) to pay for Long-Term Care insurance. Armed with that knowledge, she proposed Life Insurance with an LTC rider to address their concerns.

Female, Age 67

Rating: Standard Plus (3rd best health rating)

Death Benefit: $117,220

Monthly LTC Benefit: $4,689

Male, Age 65

Rating: Standard Plus (3rd best health rating)

Death Benefit: $103,139

Monthly LTC Benefit: $4,126

Read the full case study here.

Life Insurance Sale #3: Life w/ LTC to 65-Year-Old Female

We recently helped an agent with his client, a 65 year-old female with mild asthma (she takes Prednisone and Dexilant) and acid reflux. She's a former smoker, and has $50,000 in savings. She does NOT have a Long Term Care policy, and her husband is in average health.

She ended up getting:

- Super Preferred on Life, and Preferred on LTC rider

- Single Premium: $50,000

- Life Insurance Death Benefit: $199,712

- Monthly LTC Benefit: $7,988

Read the full case study here.

Life Insurance Sale #4: Two Options for a $95,000 CD

An agent brought a lady into my office who just had a $95,000 CD come due. She moved it into a money market account until she could figure out what to do with it.

She has 3 daughters (husband is still alive but not healthy at all).

Annuities and life insurance options were discussed, as shown below (based on 100K single premium).

Her options include:

- 5 year fixed annuity at 3%

- Life policy with Death Benefit of $219,923

(standard non tobacco for 72 female)

- Life with LTC rider, Death Benefit of $207,107.

Monthly LTC benefit of $8,284

The commission on the options:

- Annuity = $2,900

- Life = OVER $8,000

Read the full case study here.

Smokers vs. Non-Smokers

Smokers are going to pay more than non-smokers – that's just the nature of life insurance.

For example, if we look at a $20,000 final expense policy, a 65-year-old female located in the Fort Wayne, Indiana area would pay as low as $69 per month as a nonsmoker. That same female, if she was a tobacco user, would pay $93.

An 80-year-old male would pay $223 as a non-smoker, and as a smoker, that would increase to $304.

Smoking isn't cheap!

Term life is even worse with an average of a 223% premium increase just because you use tobacco.

Finally, if we look at permanent life insurance, there are typically 2 rate classes for smokers:

- Preferred Smoker

- Standard Smoker

If a 65-year-old female wants a $100,000 life insurance policy with a long-term care rider, she'd pay $180 per month as a non-smoker. If she was otherwise healthy but was a smoker, her monthly premium would increase to over $315 per month.

The only exception to this rule is the Americo Final Expense policy. They offer a Quit Smoking Advantage program that gives smokers a chance to quit before raising their rates.

Smokers can receive an Eagle Premier Smoker policy with Non-Smoker rates for the first 3 policy years. If, by the 3rd policy anniversary, they can provide evidence that they quit smoking for at least 12 months, their death benefit and premium remains level.

Training, E/O Insurance, and Contracting

In order to sell life insurance, you do need some basic training.

Step 1 is Anti-Money Laundering (AML) training.

This can be done on the LIMRA website. You just register online, and you keep it up to date on an annual basis. The test is free.

Step 2 is obtaining Errors and Omissions (E/O) insurance.

This is just something good to have, but you also are required to have it. You probably get a lot of emails about E/O insurance; the carrier you decide to go with is entirely up to you.

Step 3 is to be LTC-certified if you plan to offer Life with LTC.

Finally, if you want to sell Life with LTC, some carriers require you to be LTC-certified. John Hancock is one of those carriers, and their plans are some of the best on the market. With this, you have to take refresher courses that you do pay for. We can help you get started with this.

Step 4 is to get contracted with the carriers of your choice.

As far as contracting goes, most carriers will let you get contracted with your first app – you probably already know this is called “Just in Time.”

However, there are a few carriers that require you to be contracted beforehand including Aetna, AIG, Equitable, Foresters, Prosperity, and RNA Life.

Writing Personal Notes to Underwriters

Underwriters don’t know your client like you do. They don’t understand their goals and intentions, and it makes their underwriting job much more difficult.

The application, exam, and medical records don’t always give an underwriter the details they need in order to fully understand the client.

When you send in a personal note explaining why the client is choosing this life insurance policy along with any justifications and explanations, you’re helping that underwriter immensely.

In the personal note, you’re explaining the client and the client’s situation – basically, anything that can help the underwriter understand the client better. You should include the purpose and goal for the application along with any explanations and justifications.

Some examples of things to include might be:

- Financial explanations,

- Perhaps why a family member is the payor,

- A medication that has dual purposes in which you outline the specifics,

- Any type of medical detail that can help the underwriter better understand the client, etc.

The personal note should include your contact information, the date it was written, and it should be signed.

How to Market Life Insurance to Seniors

People realize they need life insurance. In fact, 68% of Americans in a new survey admitted they personally need life insurance. We also have Life Insurance Awareness Month every September reminding the nation that life insurance coverage is extremely important.

According to a survey done by Ladder and OnePoll, Americans don't buy life insurance because of misconceptions that can be solved by YOU, the agent!

People think it's going to be too expensive, they don't think they need it, they don't know what kind of policy to get, how much coverage they need, it's too confusing... all of this can be solved by you.

Understanding this can make it that much easier for you to market yourself as a life insurance expert.

We've also made it as easy as we can by creating some marketing pieces that you can put to use right away.

To start the conversation about Life w/ LTC, mail out this warmup letter that explains the costs of long-term care and why a hybrid option is a great solution.

We also have a slew of other marketing pieces and informational materials in our comprehensive Life Insurance Marketing Kit.

In that kit, we have several different warmup letters you can either mail out or send via email. There's a letter for prospects that don't know you yet, a variation for existing clients, and a "3 questions for existing clients" letter that is sure to pique their interest.

Beyond what we've already created, life insurance carriers also put together marketing pieces for their contracted agents to customize and use.

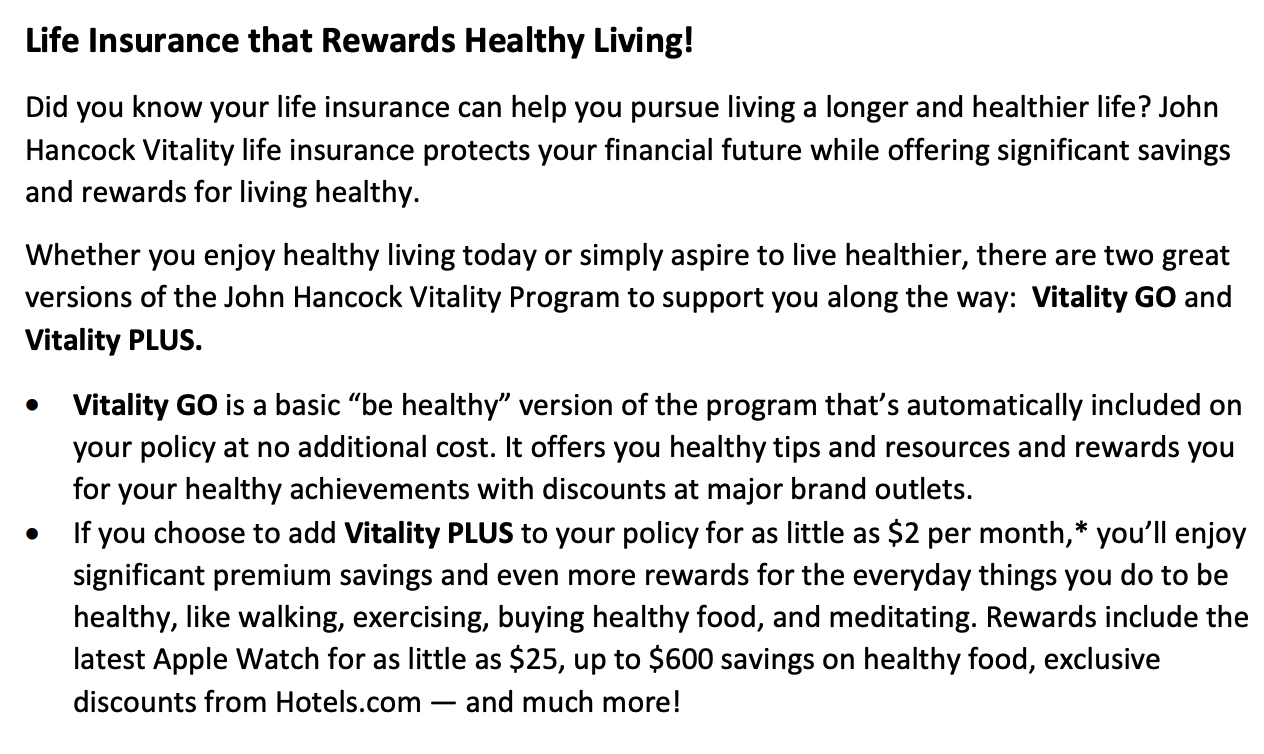

For example, John Hancock has hundreds – yes, hundreds – of sales tools for their life insurance agents. There's an email promoting the Vitality program:

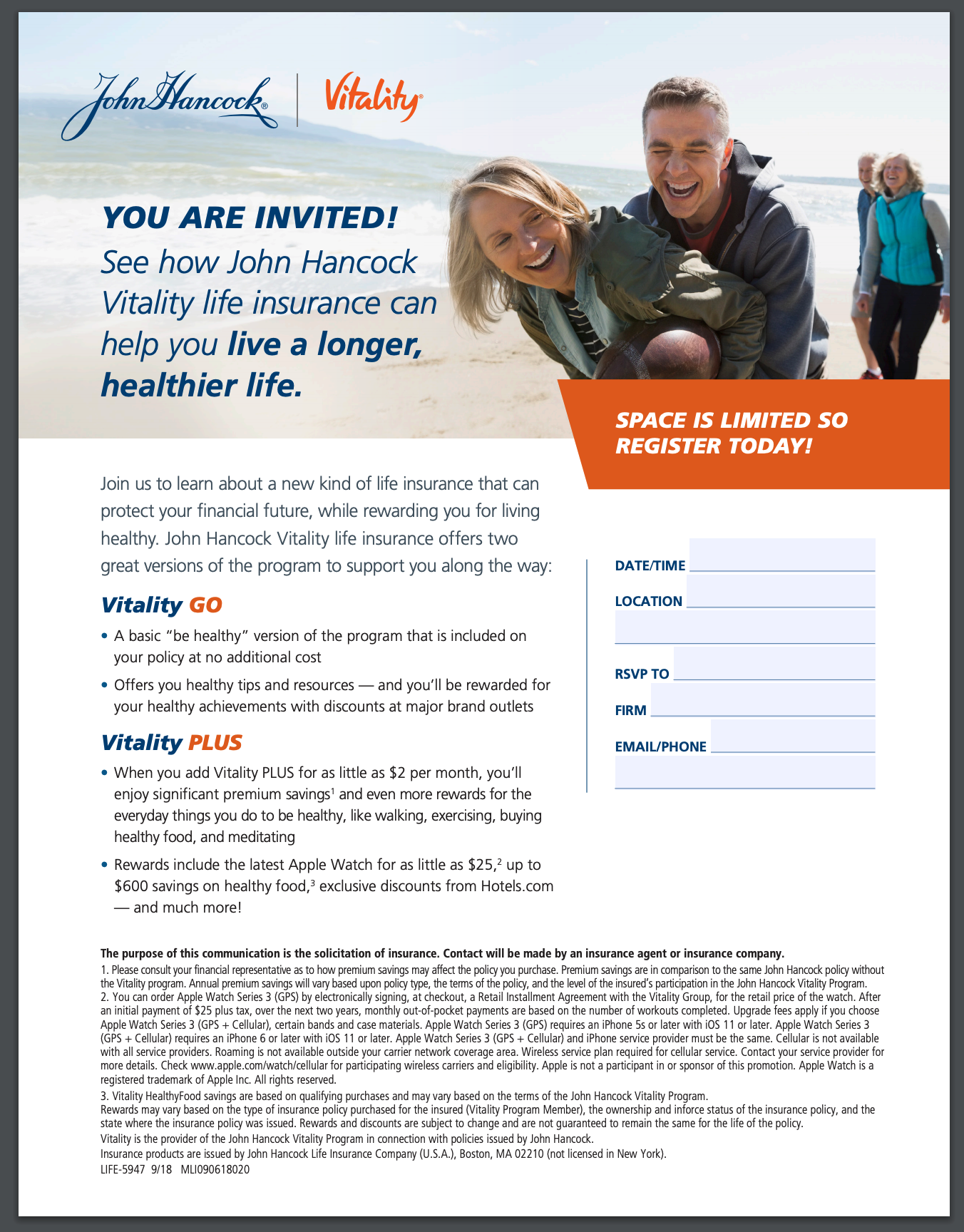

Or even an invitation to a seminar:

Many insurance carriers curate these materials for agents to use at no cost, so be sure to ask or take a look around in the agent portal!

Get Started With New Horizons

If you're ready to start selling life insurance, the next step is to find out which carriers you should choose. This depends on the state you're in as well as the type of insurance you want to offer to your clients.

As far as commission goes, I can say that life insurance sales are definitely worth your while – believe me! Take Laura Pecina, for example, who earned over $20,000 on a single Life w/ LTC case! Contact me for more information on your commission potential.

Starting out with a few carriers is a great start, and remember – you don't have to know every detail. That's what we're here for. As long as you can uncover the need and rely on us for support, you can start selling life insurance in the senior market.

Good selling!

Comments