Medicare sales can be a very lucrative career path, especially after you get through the first few years. Thanks to residual income, many agents build up a book of business that continues to pay them on policies they sold years ago.

If you've decided you want to become an insurance agent in the senior market, this is your practical step-by-step guide, starting from square one. We'll take you through the required training, licensing, contracting, certifying, and marketing.

You can also download our free eBook dedicated to new agents looking to get started on the right foot:

Without further ado, here are the 6 basic steps to complete to get started in Medicare sales.

Step 1: Complete prelicensing education.

If you've decided you want to sell Medicare products, your first step is to complete the prelicensing education requirements. Most states require you to complete and file proof of your prelicensing education in order to take the Life and Health exam.

The exact requirements vary by state. Some states allow you to do the classes online, while others require in-person.

All of the rules have shifted slightly due to COVID-19 in favor of online, but be sure to check with your state.

Different vendors offer prelicensing training classes, and that also varies quite a bit from state to state. Using Illinois as an example, we use ABRC, which offers both online webinars and in-person seminars. The training classes are two full days long, and the total cost is $285.

We checked a variety of vendors in different states, and the pre-licensing training courses can vary anywhere from $99-$400.

When you finish your prelicensing education, it's time to take your Health and Life exam.

Step 2: Take the Life and Health Insurance Exam.

Your next step is getting licensed. For what we do, you need the Life and Health license.

Several states offer their insurance exams through Pearson Vue, a company that specializes in high-stakes exams, including certifications and licensing exams.

The cost for the exam is around $50. You need a 70% score to pass, though you can retake the exam up to five times in a one-year period.

For states not offered on Pearson Vue, check your Department of Insurance website. The quickest way to get there is by doing an online search for "*your state* health and life insurance exam."

For example, Alabama offers exams through the University of Alabama in six cities across the state. The cost is $75, and you must go to the location to do the testing (it's not available online).

Step 3: Decide what products you want to sell.

Once you get licensed, the next step is to figure out what products you want to write. If you plan to get into Medicare sales, you definitely need Medicare Supplements and Medicare Advantage (more on Medicare Advantage in Step 5).

If you plan to utilize a needs assessment to structure your appointments, you'll also want to be prepared to sell a variety of products that serve the senior-aged market.

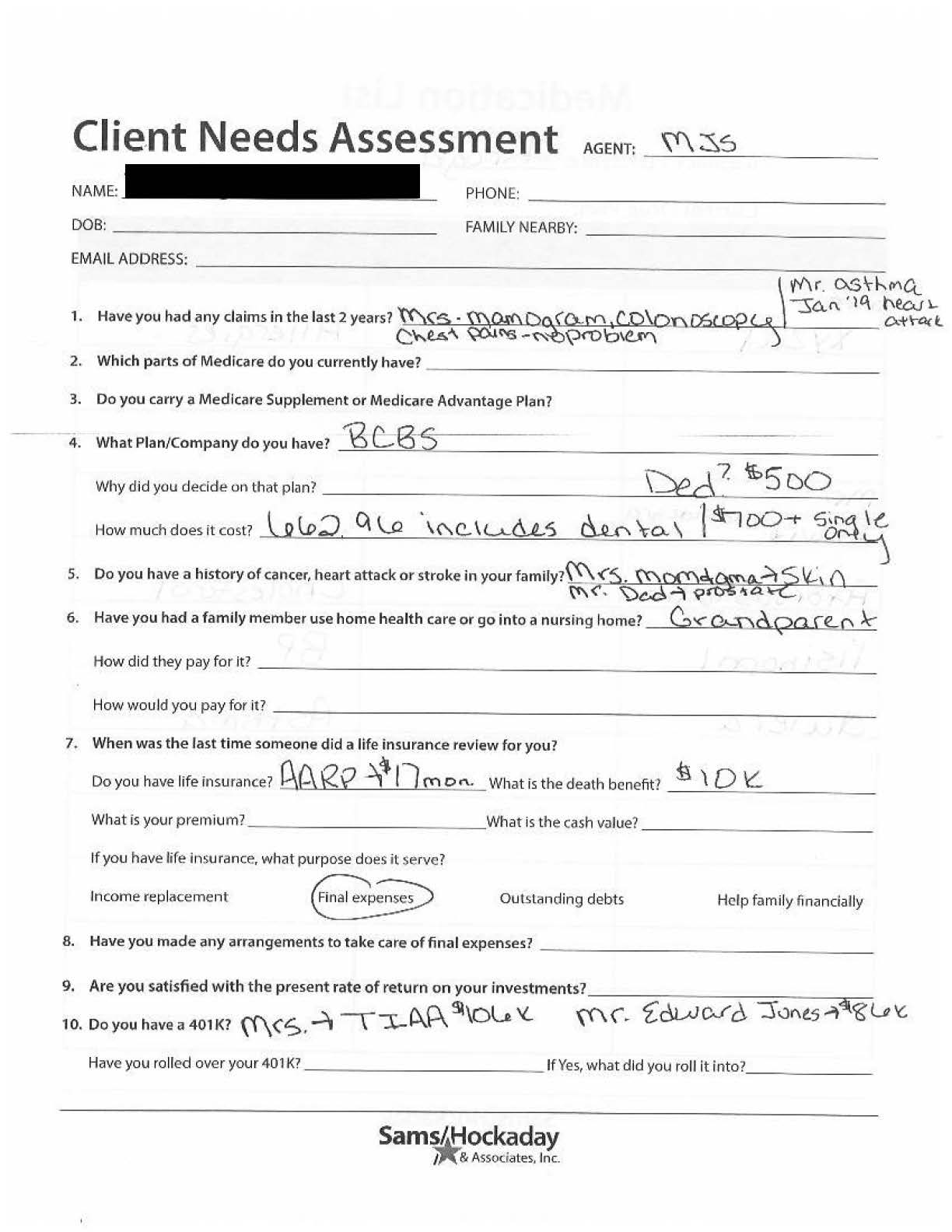

The Client Needs Assessment we use and recommend will uncover needs for the following products:

- Medicare health plan (Med Supp or Med Advantage)

- Life insurance – inlcuding final expense

- Annuities (MYGAs and FIAs)

- Cancer insurance

- Dental, vision, and hearing insurance

- Long-term care solutions (long-term care insurance, short-term care insurance, or a hybrid life policy)

- Hospital indemnity insurance (typically pairs well with a Med Advantage plan)

- Prescription drug plan (pairs with a Med Supp)

Example of the Client Needs Assessment:

Getting set up with so many products can feel overwhelming to start, so you might pick a couple to begin with. But without question, you need to be prepared to sell Medicare health plans. That's what most clients will be coming to you for.

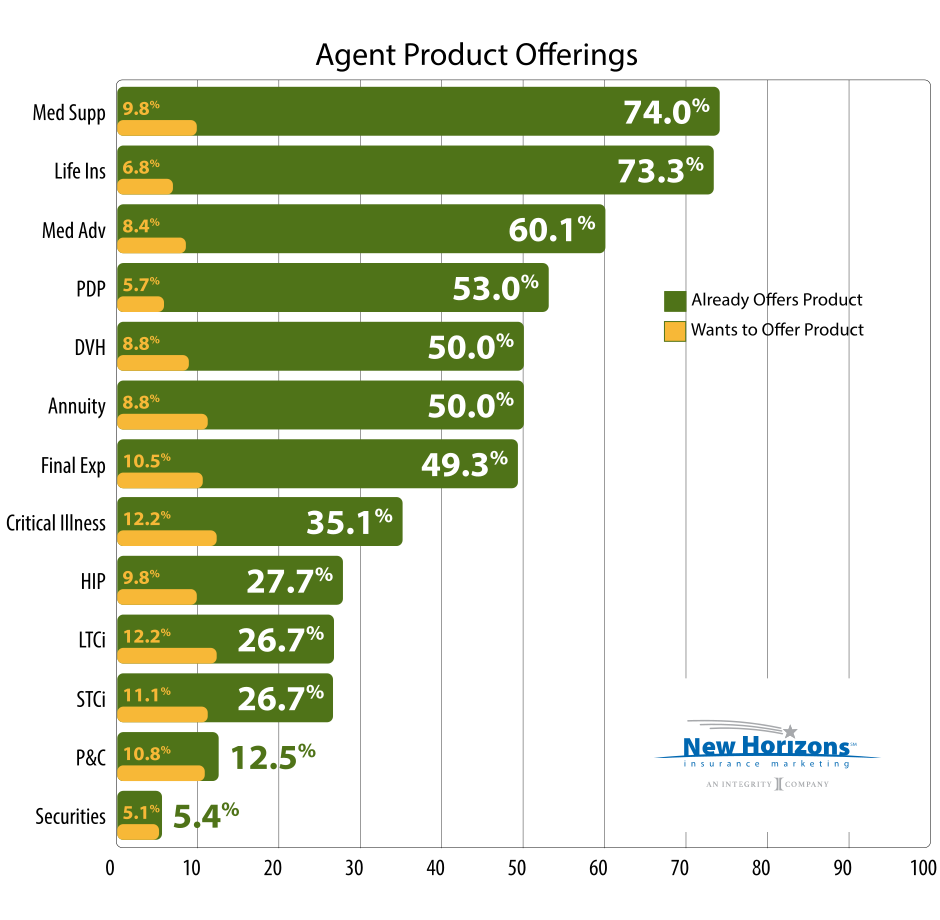

Our senior market report found that agents who make more than $200,000 annually offer six or more products. Here's a chart showing what products agents are selling, based on our survey results.

If you're a captive agent with an agency, they will provide all the training you need to get started. If you decide to go independent and run your own business, you're responsible for figuring that out.

We have a variety of free training hubs that offer product-specific training to get you started.

Step 4: Get contracted with the carriers you want to sell.

Once you decide what products to start with, you need to choose an FMO and start getting contracted.

When you're brand new, it doesn't hurt to try out a couple of FMOs so you can get a feel for which one serves you best. Give it a few months and then decide which company you really want to do business with.

Related: Can You Be Contracted with Multiple FMOs?

Ultimately, it pays to do the majority of your business with one FMO. If you divvy up all your sales, you'll be a small producer to everyone. But when you put most of your sales with one FMO, you become a power producer in their eyes and can get extra perks.

Here at New Horizons, our top agents qualify for extra incentives, exclusive training opportunities, awards and recognition, and even an invitation to an annual Agent Summit.

If you decide on trying out New Horizons, we recommend all new agents call us to talk through the contracting process and which carriers you need.

Step 5: Take the AHIP and certify with each MA and PDP carrier.

If you decide to sell Medicare Advantage (MA) or prescription drug plans (PDP), you'll need to take the AHIP. America's Health Insurance Plans (AHIP) offers an online exam all agents must take if they plan to sell and be compensated for Medicare Advantage of prescription drug plans.

AHIP's exam is CMS-compliant and costs $175. Many carriers offer a discount on the AHIP, bringing the cost down to $125. The AHIP usually opens up in June, and you can access the AHIP Medicare Training website at ahipmedicaretraining.com.

After you take the AHIP, you have to certify with each MA and PDP carrier you contract with. Because of this process, our Director of Medicare Advantage Sales recommends you make strategic decisions about which carriers you need.

He can run reports on your target counties to make the decision easy! Just schedule a free consultation with him to get started.

Step 6. Develop a marketing plan.

Now that you're licensed, certified, and ready to sell, you need to find prospects to sell to!

This is probably the hardest step for most producers, and it's why so many brand new agents fail and leave the industry. Despite 10,000 baby boomers turning 65 every single day, it can be difficult to get your foot in the door.

Get involved in your community

Our senior market report found that agents with the highest incomes say their #1 lead source is referrals. Developing local connections in your community is critical – you want to position yourself as the go-to guy or gal when it comes to all things Medicare.

Get involved with associations, affinity groups, and organizations in your area.

Some examples include:

- The VA

- Church groups

- Camping groups

- Quilt clubs

- Country clubs

- Book clubs

- Rotary clubs and other civic organizations (Elks, Lions, Moose, etc.)

- Chamber of Commerce business after hours

- College alumni clubs

- Local charities

- Homeowner’s associations

Partner with other businesses

You can also connect with other businesses in your area and develop a referral stream.

For example, you might connect with a financial advisor – she would refer her Medicare clients to you for their health and life insurance, and you would direct your clients to her for retirement planning.

You could also partner up with a local bank – they have a vested interest in people not moving their Health Savings Accounts (HSAs). They’d be happy to refer their Medicare-eligible customers to an agent specializing in Medicare Advantage plans.

Clients can use their HSA money to pay for out-of-pocket costs associated with MAPDs. You can also use your HSA money to pay for Medicare Advantage premiums (but not Medigap premiums).

Start marketing yourself

Last but not least is the massive category of traditional marketing. Set up a website, a Facebook business page, an email marketing platform, and so on.

Times are changing, but door-knocking has been a great starting point for a lot of agents. Newsjacking is also worth looking into – it's a marketing technique used by thought leaders in a community. It's essentially a way to get on the news or the radio by offering unique commentary on a news-worthy event.

We also have lots of marketing materials you can use, including email templates, sales letters, and postcards.

Frequently Asked Questions from New Agents

We actually have a full article covering common questions from new agents, but there are two that are the most popular, by far:

- How do I get leads?

- How much money will I make? / What's my commission going to be?

When it comes to leads, we don’t currently offer an internal lead program. We’ve done them in the past, but we found that occasionally, the agent could get a batch of bad leads and it would hurt our relationship with them. We don’t have control over the quality of the leads, so we decided to pay all the commission we can, and you can choose their lead source.

If you want to purchase leads, you can check out our lead vendors page. You'll get access to exclusive discounts and offers for New Horizons agents only.

And for commissions, it depends on the product and your state. For Medicare Supplements, you will make between 18-24%, and that just depends on your carrier and state. There are a couple of states that do things very differently, but 18-24% is pretty standard.

Based on our production as an FMO, we have access to the highest contracts available. That means no matter which contract you need, we're at the top of the food chain and can offer you the most competitive contract.

Related article: Get advice for new insurance agents

Advice on Selling In Multiple States

Finally, I do want to quickly go over selling products in several states. When you're just starting out, I recommend starting in one state and slowly expanding. You need non-resident licenses for states you don't live in, and those cost.

If you don't want to get a non-resident license and you need to write a policy, we can write it for you and split the commission. You'd just call us, give us your client's information, and we'll call them to finish the application. We'd then split that commission with you 50/50.

If you plan to actively market in other states, you definitely want to get your nonresident license, but it can be overwhelming to do right out of the gate.

Read more: Want to Expand Your Med Supp Business? Consider These States

Conclusion

Starting out as a brand new independent agent in senior market sales can be intimidating. It takes a couple of years to build up a book of business that provides residual income. However, if you stick with it, the sky is the limit.

Related: Is Selling Medicare Lucrative?

To recap, here are the basic steps to get started in Medicare sales: complete your prelicensing education, get your Life and Health license, decide the products you want to sell, get contracted, and start marketing!

If you have any questions or need more help, give us a call at 888-780-7676 or start a website chat during our business hours (M-F, 8am–4:30pm). Good selling!

Comments